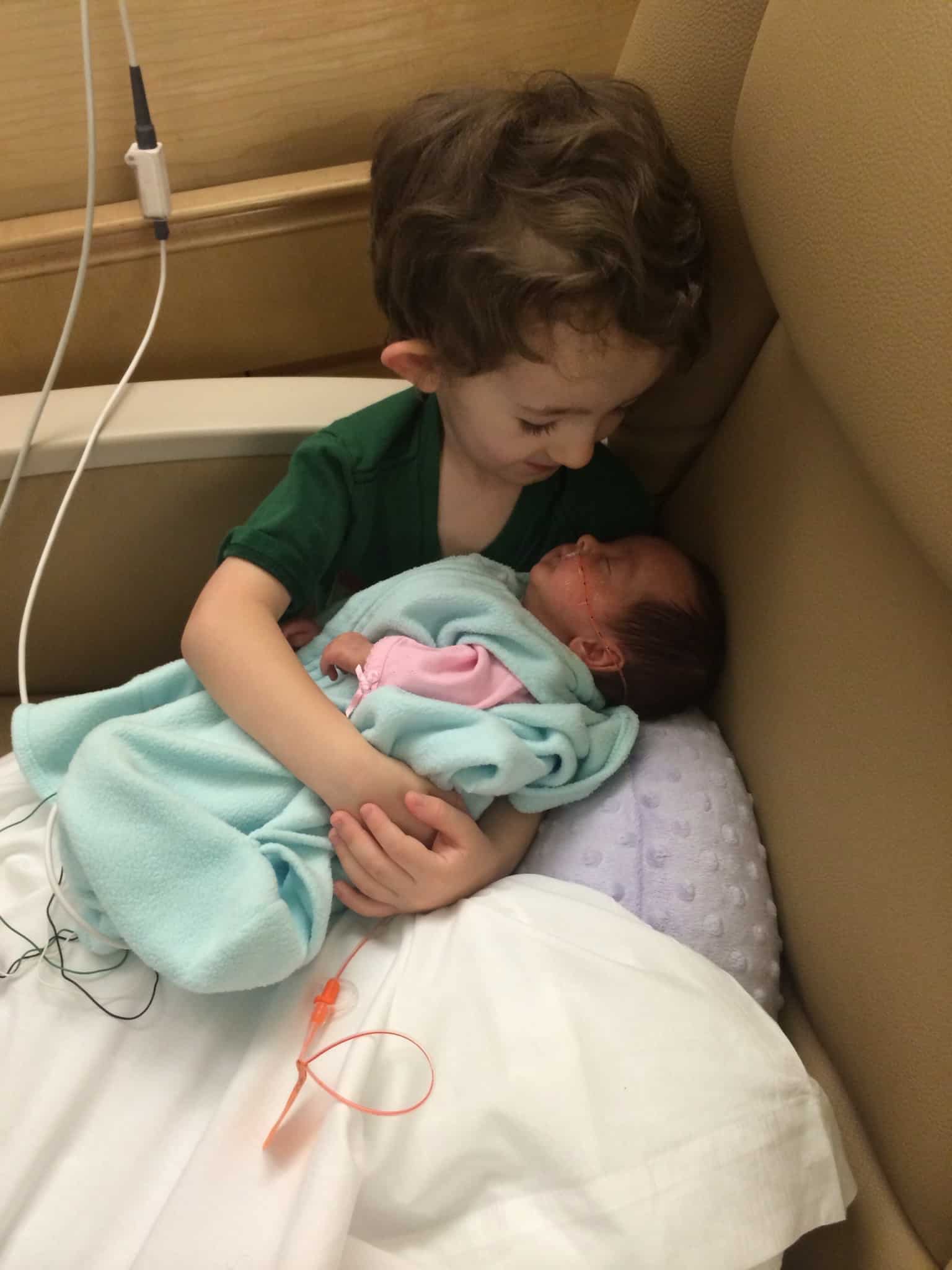

What Healthcare Looks Like For My Family…

Having a child with a rare genetic disease or a lifelong disability opens your eyes up to a whole new understanding of how medical care, prescriptions, and insurance work. Before my kids, I thought I understood… You had insurance, you had a co-pay and a deductible, and you got the treatment and medication you needed when you needed it. That was true until it didn’t work that way anymore and my husband and I were left with thousands of dollars in medical bills, and no way to afford the medication 2 of my 3 kids needed to live a normalized life.

Having a child with a rare genetic disease or a lifelong disability opens your eyes up to a whole new understanding of how medical care, prescriptions, and insurance work. Before my kids, I thought I understood… You had insurance, you had a co-pay and a deductible, and you got the treatment and medication you needed when you needed it. That was true until it didn’t work that way anymore and my husband and I were left with thousands of dollars in medical bills, and no way to afford the medication 2 of my 3 kids needed to live a normalized life.

Since my insurance provider was unable to help cover the therapy my son needed, at several points, I did try and seek help from the local school district for the developmental disabilities he was experiencing (he is the oldest of the 2 with disabilities, and the only one school age). What I found in that system was nothing but more stress and struggle. You see, they don’t view disabilities like we do. They only help children with significant delays or with diagnoses they are familiar with. They have little checklists and charts to show them who they can help. They have limited funding to meet the needs of a student like my son because they truly just don’t understand his rare disease. And that doesn’t even address the other main problem. Prescriptions.

One of the medications my children require can be in excess of $30,000 per year if insurance won’t pay. Multiply that by 2 and you can see that there is really not a way for a family to do that.

While attending an out-of-state medical convention three years ago for children with the disorder my 2 faced, I was told about a disability Medicaid based not on income but on the child’s medical diagnoses and level of care needed. When I returned home I begin asking about this and finally found out about TEFRA Medicaid. Applying was another huge process as you have to work very closely with a care coordinator. It is a multi-part process, in which you must provide proof and documentation that your child’s disabilities are considered serious enough to warrant a high level of care. The decision is in no way based on the family income or assets. They do look at the child’s assets – if any.

To further explain what TEFRA is I have copied basic info directly from the State of Alaska Department of Health and Human Services website. “The Tax Equity and Fiscal Responsibility Act of 1982 (TEFRA) is a Medicaid program designed to help children under 19 years old with costs related to their disabilities. This covers significant medical, developmental or psychiatric needs. Although they may be deemed “disabled” or have high medical costs, not all children qualify for this program.” The website continues on to touch on criteria for TEFRA Alaska Medicaid;

“To qualify, your child must meet one of the following three “level of care” criteria:

- Intermediate Care Facility for Individuals with Intellectual Disabilities (ICF/IID)

- Nursing Facility (skilled and/or intermediate) (NF)

- Inpatient Psychiatric Hospital (IPH)

Each of these categories has specific criteria, so not all children who receive one of these three levels of care will qualify for Alaska Medicaid – TEFRA.”

This level of care needed must also be annually proven to continue the TEFRA coverage for each child. The annual renewal process can be time-consuming and a little stressful. But now, thanks to TEFRA both of my children have the medication and the therapies they need covered (for now and at least the next year).

We have also elected to homeschool my son with disabilities due to the inability of the school district to meet all of his needs.

Despite having double coverage through private insurance and now the additional TEFRA Denali Kid Care program, we still run into problems receiving and keeping quality healthcare for my children.

My son has recently been removed from a therapy he needs and deserved because of insurance problems with our primary insurance provider. They request ridiculous/repetitive documentation from providers and string out payments on sessions for sometimes up to a year. Unfortunately, as our secondary insurance provider, TEFRA, cannot step in and pay these claims until after our primary private insurance company formally declines them. In this particular case, we have a $3,500 balance despite having double coverage of insurance.

Family voices matter! Thank you, Rachel, for sharing your story. We value and appreciate all you do in the special needs community.

Family voices matter! Thank you, Rachel, for sharing your story. We value and appreciate all you do in the special needs community.